State of Waste 2016 – current and future Australian trends

By Mike Ritchie – Director, MRA Consulting Group

On 16 February 2016, the Australian population reached 24 million people. Waste generation rates are a function of population growth, the level of urbanisation and per capita income[i] and Australians now produce about 50 million tonnes of waste each year, averaging over 2 tonnes per person. There are more of us and we generate more waste per person, each year.

In the period 1996-2015 our population rose by 28% but waste generation increased by 170%. Waste is growing at a compound growth rate of 7.8% /Year[ii].

On the positive side, recycling is growing at a faster rate and since 2005 we have actually seen (for the first time) a decline in tonnages of waste sent to landfill (in the most progressive States).

We now recycle approximately 58% of all the waste we generate and landfill the rest.

Fig 1. Comparison of Waste Generation and Population Growth, MRA Consulting Group, October 2015

Targets

Most governments have established recycling targets to divert waste from landfill and to capture and recover materials for the productive economy. Most readers know that almost all recycling comes at a cost to society compared to landfill.

Generally, metals, paper and cardboard and plastic (in sufficient quantities), are commercially viable recyclables. Almost all other recycling in Australia is subsidised by someone via gate fees, grants or the like. That includes most household, construction and commercial waste. Unfortunately, there is no free lunch in recycling.

It is important to point out at the start, that it is the proper role of State government to set waste policy and direction. Most governments have set Targets between 60-90% diversion by 2020[iii]. Having done so, Government’s should have the courage of their convictions and put in place the mechanisms to permit the private sector and local governments to achieve those Targets.

Fig 2. National Resource Recovery Targets, MRA Consulting Group, October 2015

It is way too easy to put out a Strategy with Targets but then not bother to create the economic or policy conditions to achieve them. For recycling to work it must be commercially viable – whether for a private business, council or other generator.

To put it another way, waste is like a river – it flows downhill to the cheapest price. For most materials the cheapest price is almost always landfill. Continuing the river analogy, diverting it to recycling requires a “weir” (a price barrier on landfill), so that the river banks up and then flows into a different, in this case a lower, price channel (relatively cheaper recycling).

Levies

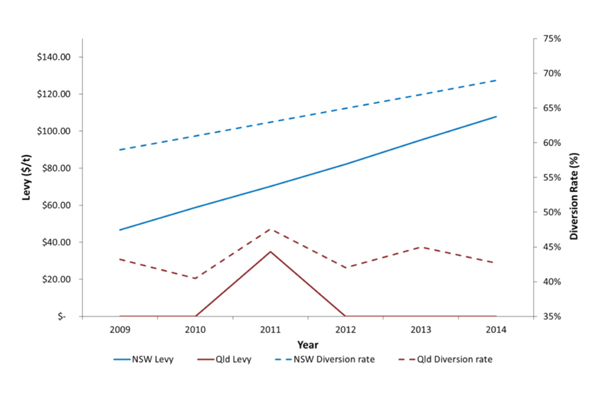

Most States have recognised this reality and introduced landfill levies to drive recycling (except QLD and NT; NT has only 1% of Australia’s waste). NSW charges a levy of $133.10/t of waste (metro), Victoria $60.52; South Australia $57 and Western Australia $55.

Fig 3. National Landfill Levies (excluding ACT, TAS and NT), MRA Consulting Group, October 2015

QLD on the other hand has no levy and total landfill costs in SE QLD are as low as $30/t, due to the removal of the levy (Fig 2), strong competition and an overabundance of landfill void space.

The effect of SE QLD’s unsustainably low landfill price has been 477,000 tonnes of waste (2014) and 398,000 (2015) travelling (by road and rail) from NSW and VIC, to QLD[iv]. The NSW Government needed to introduce the “Proximity Rule” to try to slow the flow of waste to cheap QLD landfills.

Not only did the QLD policy settings attract 15,000 heavy truck movements onto the Pacific Highway, but NSW recyclers lost the opportunity to recover materials from that stream. It was and remains, a significant unintended consequence of the removal of the $35/t levy by the (previous) QLD government.

It is important for all waste generators to understand that the levy is avoidable. It is only paid on waste actually landfilled. In other words, if you don’t want to pay the levy, then recycle.

Fix the economics of recycling

All states with compulsory levies hypothecate some proportion of the raised funds to support recycling (to lower the cost of that channel). Levies drive recycling by increasing the opportunity cost of landfill and providing funds for grants for recycling.

Taking NSW as an example, in 2013 the Government introduced the $465.7 million ‘Waste Less, Recycle More’, 4 year infrastructure and recycling services grants program. This provides real financial support for new resource recovery businesses and investment.

Testimony to the power of price, when the QLD Government introduced its $35/t waste levy (on commercial waste only) in 2013, there was an immediate spike in recycling rates. But 18 months later, after the removal of the levy, recycling rates crashed by 15% overnight and have not moved since. In the same period NSW has achieved a 16% growth in recycling (Fig 3).

Fig 4. The effect of levies on recycling rates QLD v NSW, MRA Consulting Group, October 2015

We are still a long way from achieving each State Government’s recycling targets. Further intervention via levies or other instruments such as bans, grants and regulation is required.

One of the main frustrations of the waste sector is that plenty of new recycling/recovery technology is available, the sector has the appetite for capital investment, but the main barrier remains government willingness to shift market economics. Only where recycling is commercially viable, will companies invest.

Household waste

In the household sector, consumption continues to grow with the economy. The major trends in domestic waste treatment are:

- The average garbage bin contains 60% organic material waste[v]. The bulk is food (40%) and garden waste (20%). The introduction of food/garden organic bins in many council areas will go a long way to achieving the Targets for the household sector.

- New technologies in composting and anaerobic digestion will accelerate organics diversion.

- Almost one third of all recyclable items are placed in the garbage bin and end up in landfill. Education and enforcement are the best solutions.

- Approximately 17% of households fill their recycling bin to capacity each fortnight. These households need more recycling volume usually via a 360 recycling bin.

- Many councils are also contracting Alternative Waste Technologies (AWT) to sort through the garbage bin – to recover recyclables and convert the organic component into low grade compost. These will continue to grow.

- Some minor streams including mattresses, polystyrene and batteries can now also be recycled, as a result of support by Government and the participation of charitable organisations.

There are a plethora of minor innovations but the diversion of significant tonnages of household waste will be achieved by 3 initiatives:

- 3 bin organics (or AWT processing of 2 bin systems) combined with energy from waste for residuals;

- 360L recycling bins; and

- Education to reduce leakage of recyclables and reduce contamination.

Commercial waste

In 2013-2014, the commercial and industrial (C&I) sector generated 17.13 million tonnes of waste, representing just under a third of all generated waste in Australia. Around 7 million tonnes still ends up in landfill.[vi].

By 2020, the sector will generate 29 million tonnes of waste[vii]. The effect of the levies has been to drive waste costs for most companies from 1% of operating costs towards 2-3%. Whilst these are small numbers they are a hit on EBITDA and profit.

Most businesses want to do the right thing but they are also economically rational. They will recycle to the extent limited by cost and return.

Improved technology and service offerings are contributing to improving the rate of commercial recycling outcomes. Organic materials represent over 60% of commercial waste (pallets, timber, food etc).

The major trends in commercial waste treatment are:

- Source Separated Food/Organics collections will increase with levies and grants. Only with an increased opportunity cost of landfill, can a business owner justify the increased labour and collection costs associated with separated food and organics.

- Product Stewardship will see the producer or importer, liable for the end of life disposal of ‘problem wastes’. Over the past few years, schemes for televisions and computers, oil and tyres have been introduced. Similar schemes are under review for paint, batteries, smoke alarms and gas bottles.

- Weight Based Billing for front lift skips and 240L bins etc. offers the potential for price signals to be directed at waste generators, encouraging recycling behaviour change.

- “Commercial dirty Materials Recovery Facilities” (MRFs) are now becoming commercially viable due to the rise in landfill levies, combined with new Government infrastructure grants

- Alternative waste treatment of commercial waste streams will increase with levies.

Construction Waste

Construction and demolition (C&D) waste (typically timber, concrete, plastics, wood, metals, cardboard, asphalt and mixed site debris such as soil and rocks) comprises approximately 40% of Australia’s total waste generation. The good news is that most is recycled. Recycling this material is generally cheaper than landfill and being made up of heavy materials C&D waste is particularly sensitive to landfill levy costs. As such the sector has achieved 75% recovery rates and rising, in many States.

A study released in 2013[viii] found that on average 21–30% of cost overruns in construction projects was due to material wastage. As landfill costs rise, the commercial incentive to better manage materials flow will rise, further improving recovery rates.

There are over 500 active businesses in the C&D sorting and recovery system. It is a strong supplier of jobs and resources to the productive economy.

Infrastructure

The landfill price rises are driving resource recovery infrastructure investment.

For most States the levies are now a significant revenue source. In NSW, the landfill levy raises more than $600 million per year.

To its credit, the NSW government has used these funds to establish the $465.7 million infrastructure and recycling grants program. These funds are granted to private companies and Councils (up to $5 and $10 million respectively) for new or improved recycling infrastructure.

The NSW levy combined with the grant funding, is seeding a renaissance in the development of new recycling infrastructure and job creation. VIC, SA and WA all have similar schemes though at a lesser scale. Tasmania is exploring a $10/t levy, which in turn may be used to fund future grants.

There are plenty of infrastructure solutions to achieve our aims. The most important infrastructure opportunities in 2016 are:

- Organics facilities that convert food and garden waste into compost or energy;

- Dirty MRFs to recover recyclables from mixed commercial waste;

- Automated C&D sorting platforms;

- Energy from Waste (EfW) including; pyrolysis, gasification, incineration and anaerobic digestion offering renewable energy solutions;

- Processed Engineered Fuel for export; and

- Improved household and business source separation such as 360Lrecycling bins, ‘3 bin systems’ for food and garden wastes, resident Drop Off facilities and the like.

The most important issue in infrastructure provision is that governments recognise waste as an essential service like electricity or water. The recent (2016) Infrastructure Australia report on the needs for infrastructure planning and funding, did not mention waste/recycling infrastructure once. It is a challenge we must address.

To summarise, the key reforms needed in the infrastructure space are:

- Better and faster planning processes that recognise the need for infrastructure;

- Dedicated waste zoning for infrastructure;

- Protecting buffers around existing facilities;

- Regulation of “cowboys” operating outside industry standards; and

- Recognition of the commercial imperative for investors including aggregation of waste supply, long term contracts, land availability and an approval pipeline.

Without secured long term waste supply contracts, companies cannot invest the $ millions in the advanced infrastructure that we need to further drive recovery rates.

If we wait for other forces such as innovation to lower the price below the prevailing landfill cost, then we are going to wait a long time. We must ensure that the market price signals reflect our strategic imperatives. That is the key message to governments and policy-makers.

Landfills

While the total number of active landfills in Australia is unknown, Commonwealth Government data indicates there are at least 600 mid to large sites, while there could be as many as 2,000 unregistered and unregulated landfills[ix]. The fact that, as a nation, we are unsure of the exact number of landfills in Australia, requires immediate review. Small, unlined landfills can still have significant localised impacts and probably should be registered as Contaminated Sites on relevant registers.

For the foreseeable future, landfill will remain an integral part of the product/waste life cycle. Well managed (best practice) landfills provide safe disposal of residual waste and average 50% gas capture (whole of life).

Many Council owned landfills do not price to cover the full cost of operation and remediation. Often they have been “inherited” as quarries and don’t include the cost of replacement in their pricing. This ultimately leaves an unfunded liability for residents to pick up. Similarly, the costs of rehabilitation and gas management are often left out of pricing. State governments are coming to the realisation that this needs to be remedied and have started to require landfill full life cost modelling for the setting of gate fees.

Importantly landfills also provide space for resource recovery. In fact, one of the biggest beneficiaries of landfill levies and grants has been the landfill providers who, by the nature of their business, have land with appropriate licenses for recycling.

The key reforms required in the landfill space are:

- Enforcement of minimum operating standards nationally (not just guidelines);

- A landfill accounting protocol (including post closure costs and asset replacement);

- Rationalisation of the small cut and fill trench “tips” into well run regional sites;

- Mandated gas capture for mid-sized landfills (or ERF funding); and

- Licencing and registration of all landfills in Australia.

Energy from Waste (EfW)

The Clean Energy Finance Corporation (2015), estimated that new EfW and biogas projects “could avoid 9 million tonnes of CO2-e each year by 2020, potentially contributing 12% of Australia’s national carbon abatement[x]”.

Let me repeat that. EfW can reduce Australia’s emissions by 12%. That is not including the recovery of embodied energy from recyclables nor the diversion of organics from landfill. Our agreement under the Paris Commitment (2015) was a 26% reduction in emissions by 2030. The waste and recycling sector could do most of the heavy lifting (at a low marginal cost).

There are at least 40 biomass energy plants in Australia.

NSW, VIC and WA have given the green light to EfW via new policies. These generally have 3 preconditions:

- EfW must not cannibalise recycling;

- Plants must meet high air emission standards; and

- Plants must be bona fide energy generators (not just waste disposal).

With the relaxation of State controls on EfW policies we are seeing the emergence of large scale proposals for incineration and gasification of mixed residual waste. These will act as a competitor to landfill and will further reduce Australia’s emissions. Eight large scale proposals are currently before approval agencies, with many more under development.

It is quite reasonable to expect that EfW will progressively replace landfill as the final disposal option for residual waste. However, this will occur over a 40-year time horizon, not a 4 year horizon.

Jobs

Recycling jobs are largely recession proof. Recycling rates do not generally swing as high or as low as the broader economy and much less than sectors such as mining, tourism and construction.

There are over 50,000 people directly or indirectly employed in the $14+ billion waste sector. The more we grow recycling, the more we employ people at an average ratio of 3:1 recycling:landfill[xi]. It should be noted that this ratio jumps significantly in some recycling enterprises, with some Tip Shops achieving ratios of 30:1.

These are green, sustainable jobs covering technical (engineering, chemistry, science), commercial (sales, business) and operational skills. Recycling is one of the few manufacturing sectors still growing in Australia. We need to reinforce its job creating potential.

Role of Government

The role of government (particularly State Government) is to clearly articulate where on the “recovery spectrum” they intend to sit (low cost landfill and lower recycling rates; or vice versa) and then to develop the appropriate policies, regulations and funding arrangements to make it happen.

It is clear that Australian governments are generally committed to a future of less waste to landfill and more resource recovery. However, there are significant disparities in effort and effectiveness between jurisdictions. Levies range from $0-133/t in different States and licencing and approval processes are vastly different. Some States are pursuing bans on products, others extended producer responsibility and others grants and incentives.

The National Waste Policy provides an agreed overarching framework. It needs to be dusted off, strengthened and delivered by a partnership of Federal and State jurisdictions. Progressive alignment of jurisdiction policy will facilitate reform. But ultimately market intervention through regulatory or price signals at the State level, is needed to drive large scale reform and therefore to hit State Targets.

MRA has worked with businesses and governments across Australia to create realistic waste strategies and action plans.

In our experience most businesses and households support higher recycling rates and somewhat higher landfill levies, but only where a significant amount of the levy revenue is hypothecated to recycling infrastructure and systems.

As one Councilor put it to me “No-one likes paying taxes but better they be progressive taxes than not. Better that we tax pollution and improve recycling, than tax payrolls and increase unemployment.”

With that sentiment in mind we are on the right path. Recycling rates are rising, alternative technologies are emerging, infrastructure is being built and with it jobs and economic returns. However, the fact is we are underperforming relative to State Target expectations.

This is the fourth edition of MRA’s State of Waste. If you are interested in reading previous editions of the annual review, see 2015, 2014 and 2013.

Mike Ritchie is the Director of MRA Consulting Group. MRA specialises in waste, resource recovery and carbon. MRA provides advice to companies and all levels of government. For more information, call 02 8541 6169 or email info@mraconsulting.com.au.

We welcome your feedback on this, or any other topic on ‘The Tipping Point’.

[i] Blue Environment & Randell Environmental Consulting 2013, ‘Waste generation and resource recovery in Australia P321 Final report’.

[ii] National Waste Policy 2010. Federal Government

[iii] MRA State of Waste Presentation, October 2014

[iv] State of Waste and Recycling in QLD 2015. Qld Government

[v] Food Waste Fast Facts, http://www.foodwise.com.au/foodwaste/food-waste-fast-facts/

[vi] Inside Waste Industry Report 2014-2015

[vii] MRA State of Waste Presentation, October 2014

[viii] Udawatta A, Zuo J, Chiveralls K and Zillante G, Improving waste management in construction projects: An Australian study, Resources, Conservation and Recycling 101 (2015) 73–83

[ix] MRA Consulting, Inside Waste, Strategy & Planning 2016

[x] http://www.cleanenergyfinancecorp.com.au/media/107567/the-australian-bioenergy-and-energy-from-waste-market-cefc-market-report.pdf

[xi] South Australia’s Waste Strategy 2011-2015

This article has been published by the following media outlets: